New York Financial Literacy Statistics

The New York Financial Educators Council (NYFEC) regularly collects and maintains data to explore the financial health of New Yorkers. New York financial literacy statistics appear on this website and are updated as needed to keep them current. The NYFEC provides this information to inform policymakers, researchers, organizations, and individuals for the purpose of advocating for, proposing, and implementing financial literacy policy. The organization’s overarching goal is to give the financial wellness movement forward momentum.

Cost of Financial Illiteracy Survey

New Yorkers report that lack of financial knowledge carries a high cost, according to this 2021 survey. Participants across the state responded to the single question: “During the past year (2021), about how much money do you think you lost because you lacked knowledge about personal finances?” The results are shown below. Interestingly, almost 9% of survey respondents believed they had lost $10,000 or more in the past year due to financial illiteracy (percentages are rounded).

Cost of Financial Illiteracy

$0 – $499

$500 – $999

$1,000 – $2,499

$2,500 – $9,999

$10,000 +

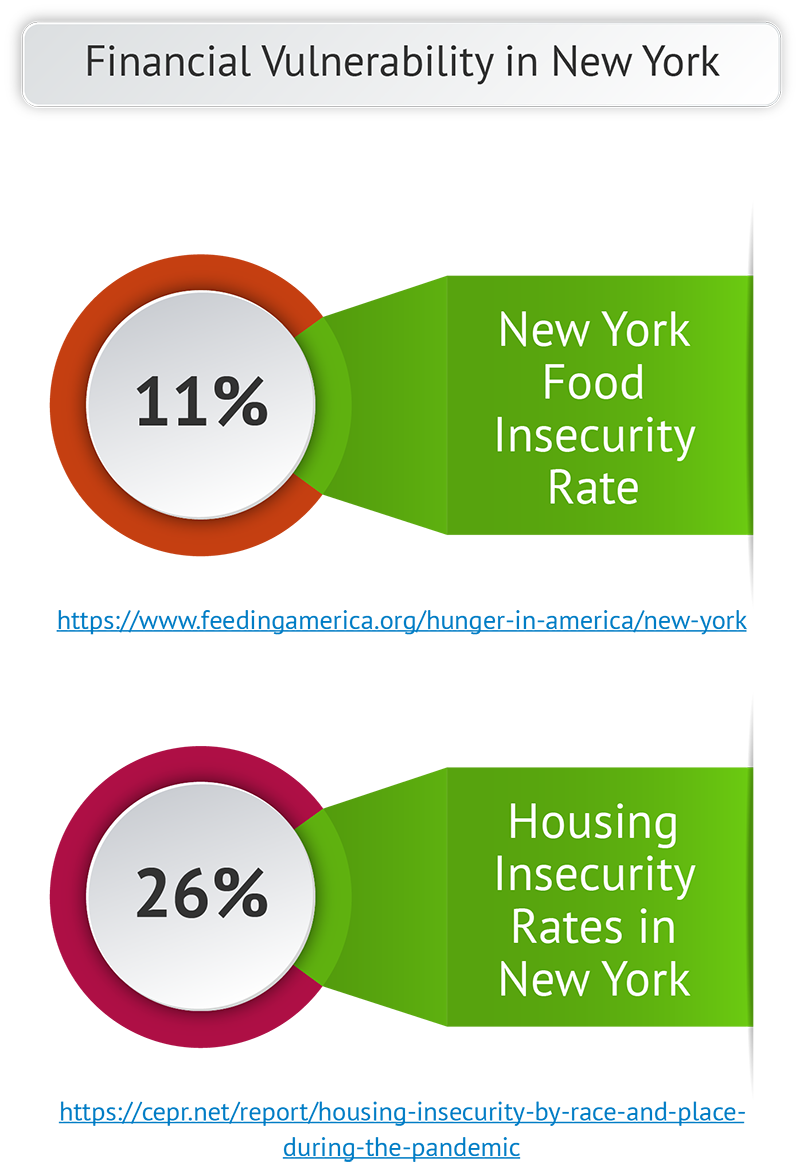

Almost 2.3 million New Yorkers face food insecurity, Feeding America reported in 2021. That figure represents 1 in every 9 New York residents, and 1 out of every 6 children in the state. One-third of those receiving help through the Supplemental Nutritional Assistance Program (SNAP; formerly called food stamps) have children in the household.

Housing insecurity in the Empire State also poses a problem, according to a 2021 report by the Center for Economic Policy & Research. The report indicated that 7.27% of New York homeowners were facing probable foreclosure, while 38.37% of renters were likely to be evicted. The combined rate was 26.29%. Measures of housing insecurity include lack of affordability, poor quality of shelter, and unsafe conditions.

Financial Situation Data

Debt Load Rates

The Empire State ranks 11th in the nation in terms of household debt, according to data reported in Forbes Advisor in 2023. The average New Yorker carries $56,590 in debt – 71.13% of the average annual household income in the state (all sources combined).

A deeper dive into the data shows that New York ranks fourth highest in the country for credit card debt alone. New York residents carry an average of $8,964 in credit card balances as of 2023, an increase of $375 over the previous year. Further, Experian reported that New Yorkers’ balance on auto loans on average was $19,090 in 2022, up 9.1% from 2021 figures; and the average home mortgage outstanding balance in the state was $271,284. Although New York residents overall were less likely to have student loan debt, those who did carry student loans had a higher average balance ($37,678) than their peers in 2022.

Personal Credit Score

Average credit scores ranked relatively high in New York as of 2023. According to Experian, New Yorkers have an average FICO® score of 721, seven points above the 714 national average. And Equifax calculates the 2021 New York average VantageScore® at 712, compared with the national average of 698.

The median credit scores of five mid- to large-sized New York cities according to WalletHub are shown at right.

New York Financial Literacy Legislation & Educational Stats

Educational data for each U.S. state are updated annually in the Common Core of Data (CCD), a report compiled by the National Center for Education Statistics – a branch of the U.S. Department of Education. The most recent CCD report (2021-2022) shows that New York had 4,802 schools operating within 1,058 districts. The total student membership in public school that year was 2,548,490; they were taught by 215,092 teachers, representing a promising pupil-to-teacher ratio of 11.8.

In its 2021-2022 session, the NY State Assembly passed Assembly Bill A976, which directed the state’s department of financial services and consumer protection division to conduct a study and make recommendations about consumer awareness and financial education in the state. The bill also directs the state financial services website to publish “information to enhance consumer financial literacy and consumer awareness which shall include information on basic banking and personal financial management, how credit scores are determined and ways to establish good credit, options for investing and increasing savings, best practices for protecting personal information, and any other topics deemed appropriate by the superintendent” by January 2022. Although several bills to require a standalone financial education course in high schools have been introduced in recent years, none has passed to date.